Credit Union Participations and Servicing

Expand your participation strategy with secured private credit backed by commercial real estate collateral—supported by underwriting discipline, servicing infrastructure, and reporting tools designed for internal governance.

Credit unions diversifying earning assets beyond a local footprint through participations

Teams managing loan-to-share optimization and concentration risk

Institutions seeking workflow support across diligence, servicing, and reporting

Governance-driven organizations requiring permissioned access to diligence materials and ongoing portfolio visibility

How AVANA helps credit unions

- Credit unions diversifying earning assets beyond a local footprint through participations

- Teams managing loan-to-share optimization and concentration risk

- Institutions seeking workflow support across diligence, servicing, and reporting

- Governance-driven organizations requiring permissioned access to diligence materials and ongoing portfolio visibility

Conventional Loans

We carefully design our loans with the needs of Credit Unions as our top priority. We focus on risk mitigation to generate attractive risk-adjusted returns. We also plan for holdbacks or earnouts to keep our partners in a comfortable financial position.

Government Guaranteed Loans

AVANA has extensive experience managing loans backed by government programs like SBA 504, 7a, and USDA. These programs are valuable as they provide businesses with essential capital and offer significant credit enhancements to lenders.

Portals to Support Your Investment Workflow

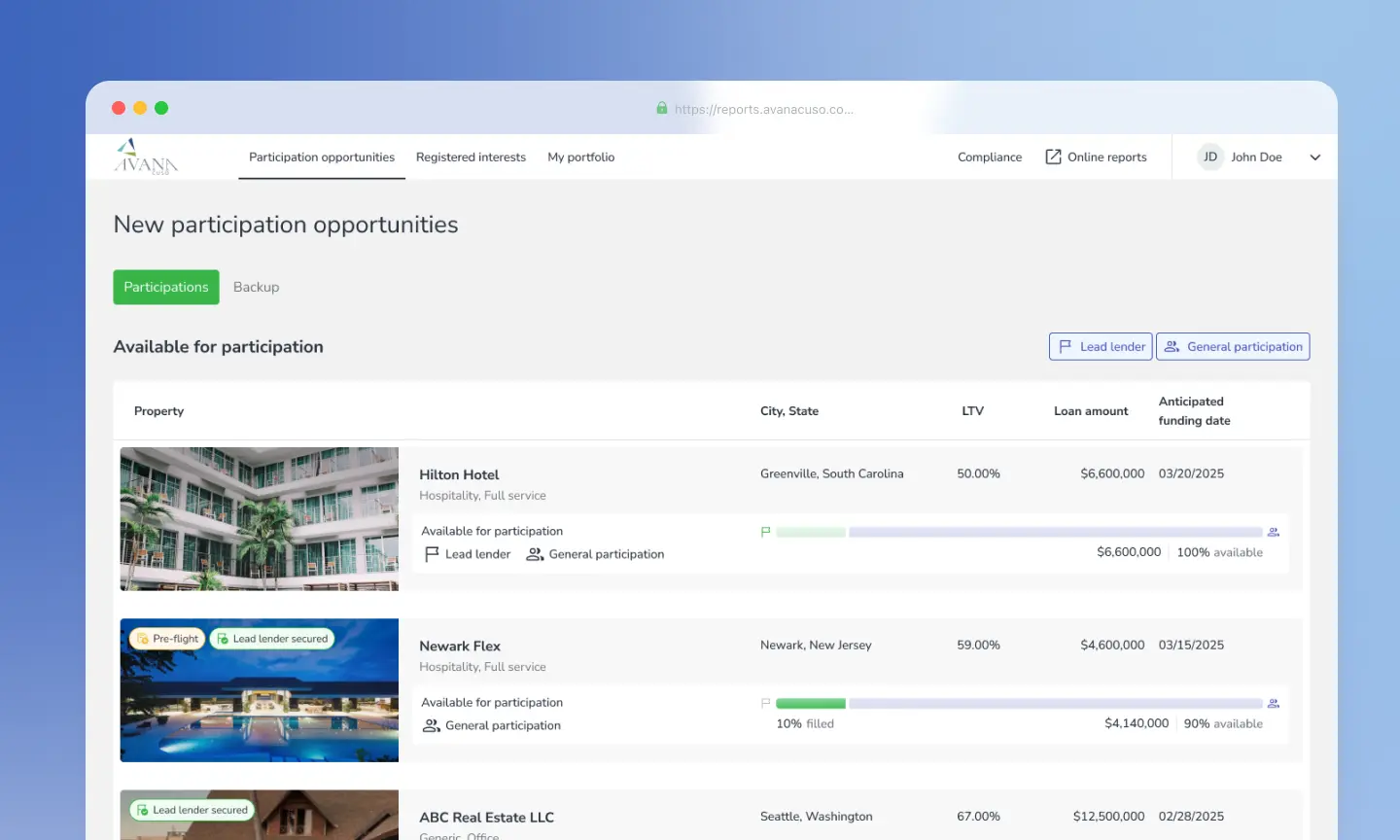

Participation Desk

A platform designed to streamline access to commercial real estate (CRE) loan opportunities, with controls that support internal workflows:

- Lending preference management to align opportunities with strategy

- User management to support internal controls

- Email notifications to keep stakeholders informed

Find Opportunity to Invest →

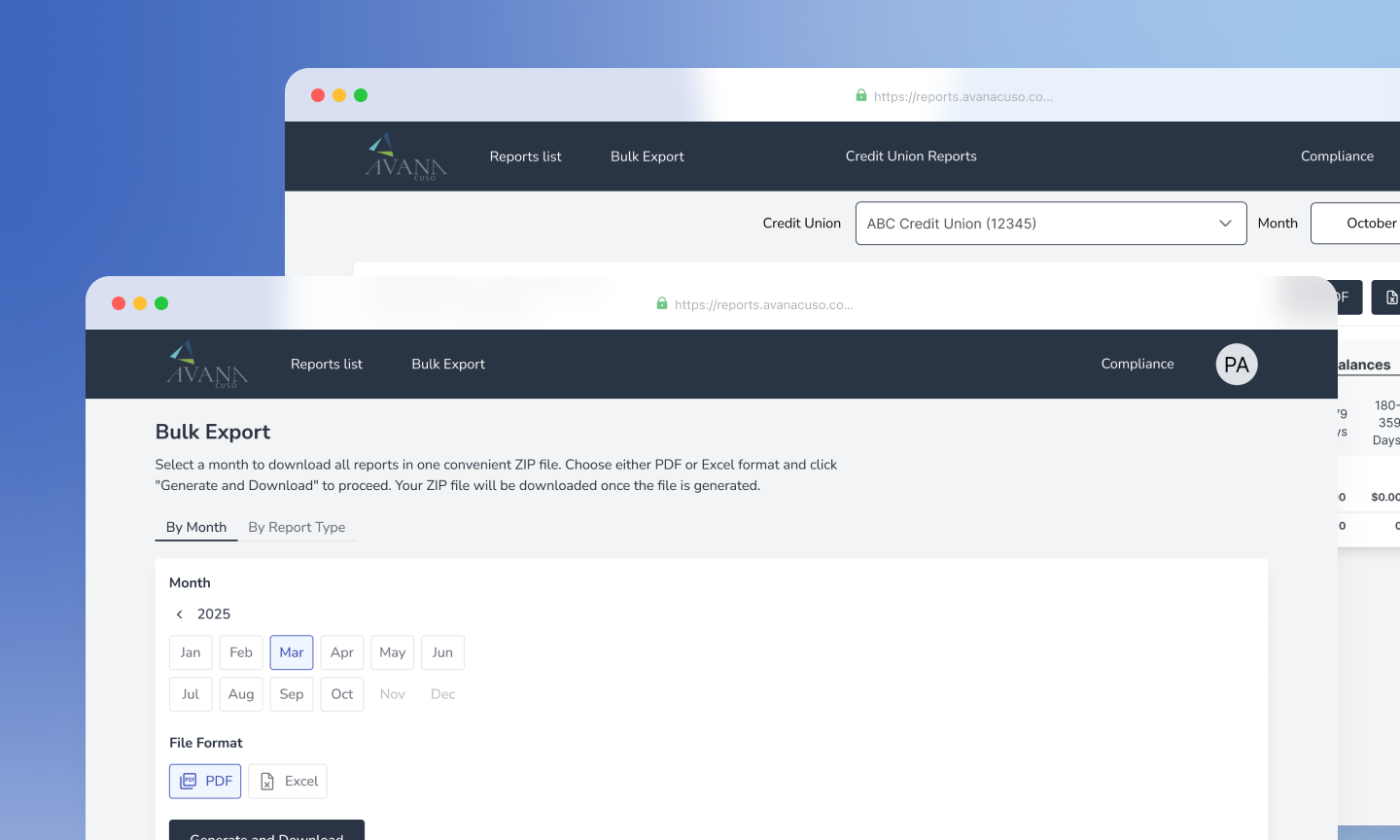

Reporting Portal

Tool designed for ongoing visibility and governance-friendly reporting access

- 24/7 access for on-demand visibility

- On-screen viewing, or Excel/PDF export

- User management and role-based access

- Granular report access to support internal governance

Login to Reporting Portal →

How to invest with AVANA

Connect

Review

Due Diligence

Onboard

Invest

Monitor

Pre-screening

Underwriting and diligence

Documented decisioning

Closing controls

Ongoing monitoring

Compliance procedures

What guides our decisions

Key factors we use to guide our decisions:

Credit discipline

High quality, rigorous and consistent risk approach from origination to portfolio mangement

Embedded risk control

Documented diligence and mitigants where appropriate

Focused specialization

Sector expertise and asset-level evaluation in select markets

Fundamentals first

Decisions grounded in cash flow, sponsor strength, and obligor capacity—not market timing

Purpose & alignment

Capital deployed with mission focus and alignment of interests, subject to offering terms

Reporting & Transparency

- Lender statement of account: typically provided by the 15th business day of each month

- Loan review inquiries: typically available beginning the 16th business day following statement release

- Audit balance confirmation: annual

- Trade documents/capital calls: trade documents available for each trade (as applicable)

- Investor correspondence: made available as needed

Frequently asked questions

Proven Success Stories

We’ve helped businesses across industries

.webp)

Invest with AVANA

Insights

Our Team

About Sanat Patel

As Chief Lending Officer at AVANA Companies and Chair of the Board at AVANA Bank, Sanat Patel brings more than three decades of experience in financial services, private credit and commercial banking, with a proven track record in loan structuring, risk management, and balance sheet growth. Sanat has led strategic initiatives that connect institutional capital with entrepreneurial ambition, supporting the growth of businesses, and owners engaged in commercial real estate across the U.S. He has built and scaled lending platforms in partnership with banks and credit unions, developing tailored financial solutions that drive job creation and foster inclusive economic development.